10 Documents Every First-Time Home Buyer Must Track Before Closing

The 10 documents lenders, agents, and attorneys need from you before closing — what each is, when it's due, and how to keep track without losing anything.

Published June 3, 2026

The home buying process generates more paperwork than most people expect. Between pre-approval and closing, you will be asked for dozens of documents by your lender, agent, attorney, and title company — often with overlapping deadlines, different formats, and no single place telling you what is missing.

Missing or delaying any one of these documents can push your closing date. Here are the 10 that matter most, what each one is, and when to have it ready.

1. Pre-Approval Letter

Your pre-approval letter is the document that proves to sellers you are a qualified buyer. It comes from your lender after they review your credit, income, and assets. Most offers without one get ignored in competitive markets.

Keep a current copy on hand — pre-approval letters typically expire in 60-90 days, and if your search extends past that window, you will need to refresh it.

2. Two Years of W-2s or Tax Returns

Lenders require proof of stable income. If you are a W-2 employee, this means the last two years of W-2 forms. If you are self-employed or have 1099 income, lenders want two years of federal tax returns including all schedules.

Gather these before you submit your formal mortgage application. Delays in providing tax documents are one of the top reasons underwriting timelines extend.

3. Two Months of Bank Statements

Underwriters need to verify that the funds for your down payment and closing costs exist and have been in your account — not gifted or borrowed last week. Have the last two months of statements for every bank account you plan to use.

If there are large deposits in those statements, be ready with a paper trail explaining them. Unusual deposits trigger lender questions.

4. Gift Letter (If Applicable)

If any portion of your down payment is a gift from a family member, your lender will require a signed gift letter from the donor stating the amount and confirming it is a gift with no repayment obligation. This is a hard lender requirement — not optional.

5. Purchase Agreement

The signed purchase agreement (your offer, accepted by the seller) is the document that starts the clock on your mortgage application, inspection period, and closing timeline. Every other deadline references the executed purchase agreement date.

File this immediately upon acceptance and make sure your lender has a copy the same day.

6. Inspection Report

Your home inspection report is typically 40-80 pages. The important parts are the summary section (items the inspector flagged as safety hazards or significant defects) and any items that trigger a negotiation request to the seller.

Track which items you requested repairs for and the seller’s response. These become part of your closing documentation.

7. Proof of Homeowners Insurance

Lenders require proof of homeowners insurance before they will fund the loan. You cannot close without it. Get at least three quotes in the weeks before closing and bind your policy at least 10 days before closing day.

Your lender’s title company will specify exactly what they need, but a declaration page showing the coverage amount and annual premium is the minimum.

8. Title Commitment

Your title company will issue a title commitment documenting who legally owns the property and whether there are any liens, easements, or encumbrances that need to be resolved before closing. Read it carefully — or ask your attorney to review it with you.

Issues found in the title commitment need to be resolved before closing. The earlier you review it, the more runway you have.

9. Closing Disclosure (CD)

Your lender must provide the Closing Disclosure at least 3 business days before closing. It shows the final loan terms, closing costs, and cash required to close. Compare it line by line against the Loan Estimate you received when you applied.

Discrepancies between the LE and CD should be flagged to your lender immediately. Some changes are allowed; others indicate an error.

10. Cashier’s Check or Wire Confirmation

Closing costs and your remaining down payment must arrive as certified funds — a cashier’s check from your bank, or a verified wire transfer. Personal checks are not accepted.

Know your exact cash-to-close amount (from your CD) at least 48 hours before closing. Wire fraud is a real risk — always confirm wire instructions by phone with your title company, never via email alone.

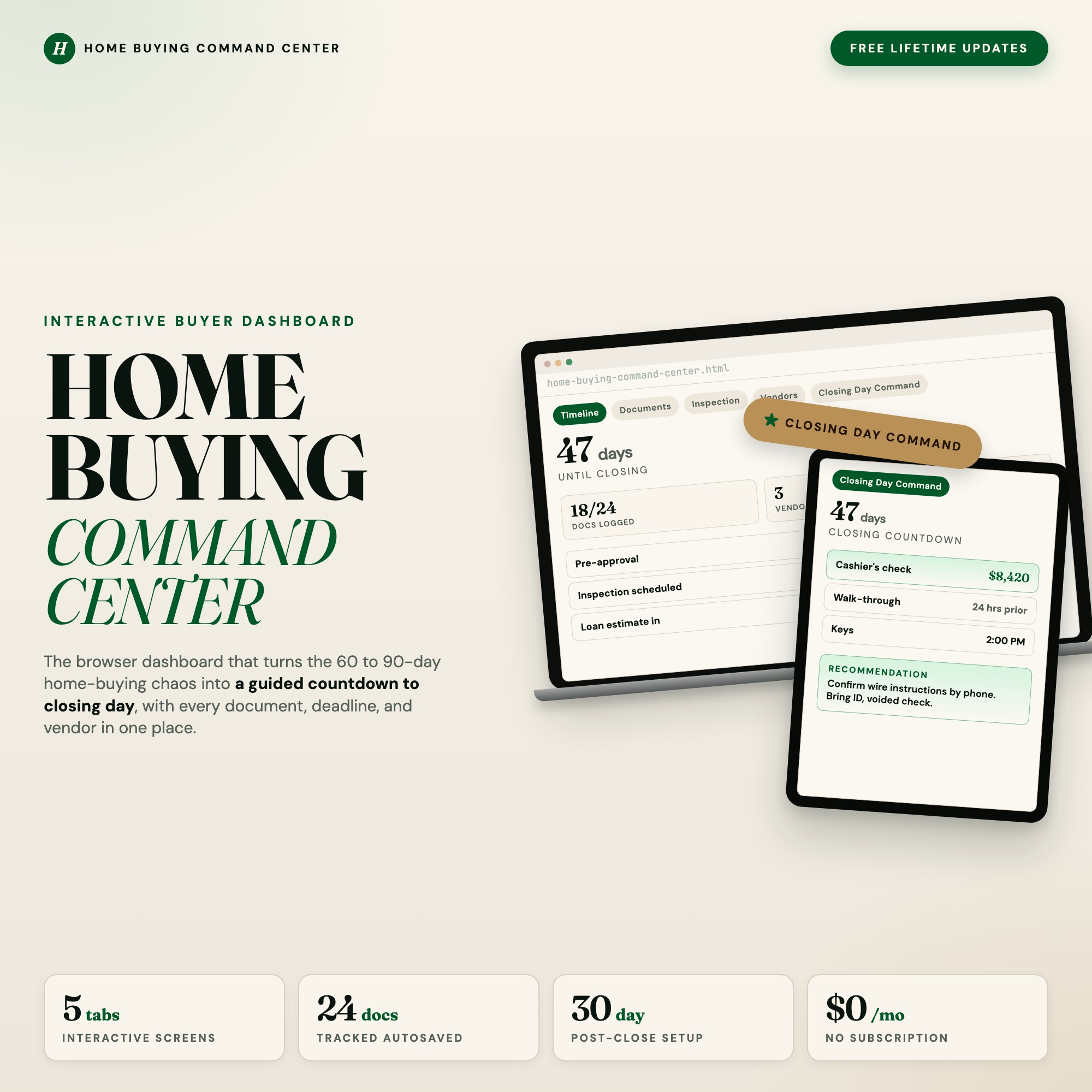

Tracking all 10 of these across a 60-90 day process is where first-time buyers consistently drop the ball. The First Time Home Buyer Planner is an interactive browser dashboard with a dedicated document tracker showing status chips (Needed, Uploaded, Approved) for all 18 standard closing documents, plus a Closing Day Command tab with a live countdown and day-of checklist.

Available on Etsy for $29 — one-time download, works in any browser, no subscription.

Frequently asked questions

- What happens if I miss a document deadline during the home buying process?

- Missing a lender document deadline can delay your clear-to-close date, which can push closing and potentially breach your purchase contract. Lenders typically give 24-48 hour notice but the cascade effect is fast.

- Do I need to spend a lot of money on tools?

- No. The First Time Home Buyer Planner costs $29 as a one-time purchase — less than two months of most subscription tools. And it is purpose-built for your workflow.

- What makes an offline HTML dashboard better than a subscription app?

- Cost (one-time vs. monthly), privacy (your financial documents stay on your device), and reliability (works without internet). The Closing Day Command tab also includes a live countdown to closing date that no generic app provides.

- How quickly can I get started with the First Time Home Buyer Planner?

- Under 5 minutes. Download the file, open it in any browser, and start using it immediately. Everything autosaves automatically.

Featured dashboards from this list

Interactive HTML dashboards — one-time purchase, works offline, no subscription.

ListingResearchOS Shop

All dashboards — single file, yours forever

Interactive HTML. No subscription. Works offline in any browser.

Browse the Etsy Shop →