First-Time Home Buyer Closing Checklist: What to Bring and Track

What to bring to closing, what documents to track during escrow, and how to avoid the paperwork mistakes first-time buyers most commonly make.

Published June 3, 2026

Buying a house for the first time means managing a process that most people do once in their life, under time pressure, with significant financial stakes. There are 15–20 documents to track, multiple vendors who need different things at different times, inspection findings to evaluate, and a closing day that requires specific preparation to not turn into a panic.

This checklist covers what to track at each stage and what to have ready on closing day.

The Document Timeline: What You’ll Need and When

Documents arrive in roughly this order during a purchase:

At offer / under contract:

- Signed purchase agreement

- Earnest money receipt

- Home inspection ordered

During inspection period:

- Inspection report (usually within 48–72 hours of inspection)

- Repair request submitted to seller

- Seller’s response to repair request

- Signed repair addendum (or no-repair acceptance)

During mortgage processing:

- Loan estimate (within 3 business days of application)

- Bank statements, W-2s, pay stubs (your lender will give you a specific list)

- Gift letters if any down payment funds are a gift

- Appraisal report (ordered by lender, paid by buyer)

- Title commitment from the title company

Before closing:

- Homeowner’s insurance binder (required before close)

- Clear to Close from your lender

- Closing disclosure (at least 3 business days before closing — federal law)

- Final walk-through completed

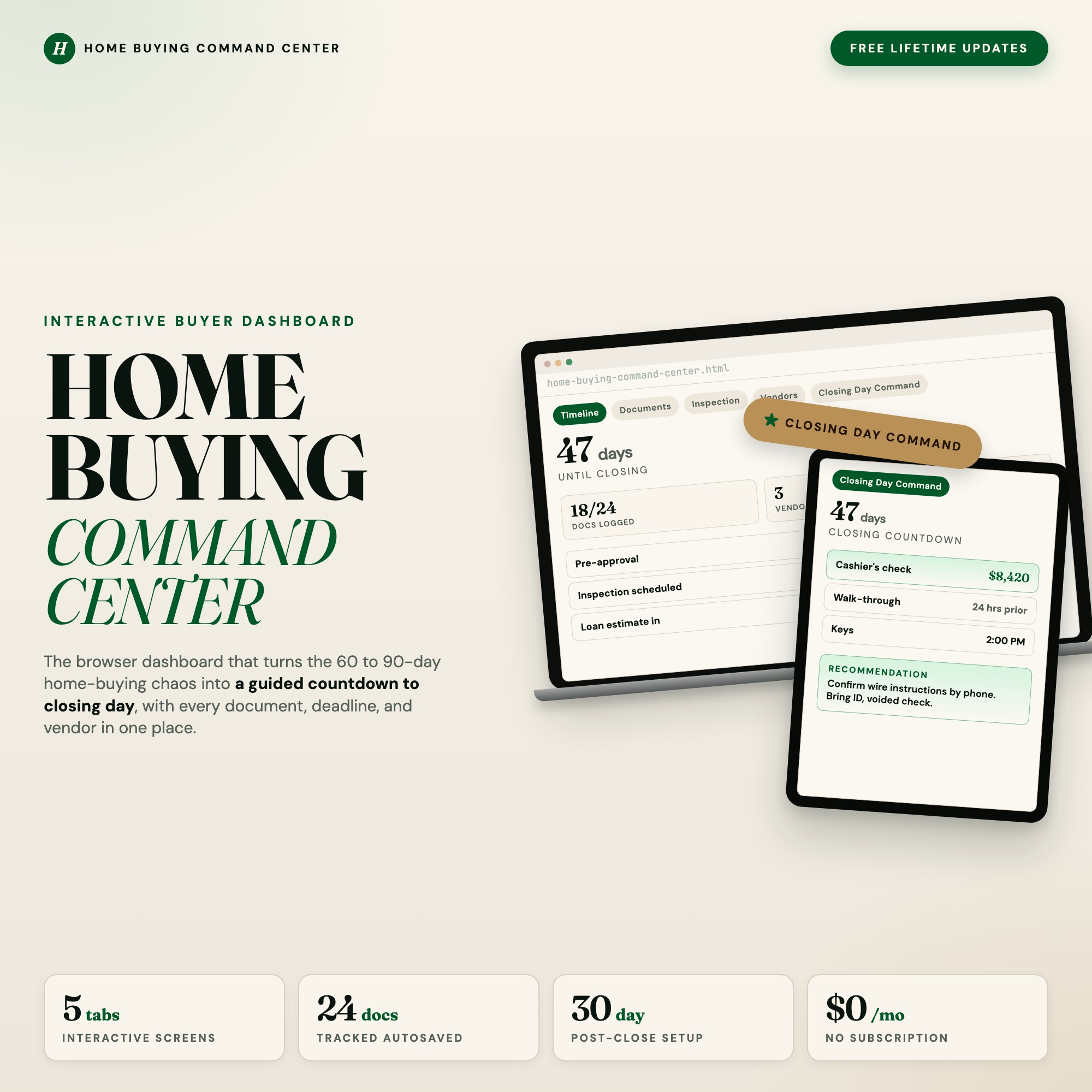

The Documents tab in the First Time Home Buyer Planner tracks all 18 standard documents with a status chip per document: Needed, Uploaded, or Approved. A progress ring shows how close to “ready” you are at any point.

What to Track During the Inspection

Your inspection report is 30–60 pages of findings. Most of them don’t matter. Here’s how to categorize what the inspector found:

Must negotiate (safety or structural): Electrical panel issues, knob-and-tube wiring, HVAC not functional, evidence of water intrusion, foundation concerns, roof near end of life

Should negotiate (expensive to fix): Water heater age, HVAC age, plumbing type, evidence of previous pest damage

Low priority: Minor cosmetic issues, easily replaceable fixtures, deferred maintenance items visible before you made your offer

The Inspection tab in the First Time Home Buyer Planner has a room-by-room checklist with a photo notes field for each item and red-flag callouts that surface the critical issues. The goal is a clear list of what you’re requesting the seller repair or credit, not a 47-page document.

What to Track About Your Vendors

A typical purchase involves: your buyer’s agent, your lender (loan officer + processor + underwriter), the title company, the home inspector, possibly a real estate attorney (required in some states), and your homeowner’s insurance agent. They each need different things from you at different times, and they’re all communicating with each other while you’re trying to manage your day job.

The Vendors tab keeps a rolodex: contact info, role, current status, and quote history. When your lender’s processor emails you requesting two months of bank statements for the third time, you have their direct contact information immediately available rather than digging through your inbox.

Closing Day: The Specific Preparation

Your lender will provide the exact cashier’s check amount 24–48 hours before closing. This is not an estimate — it’s a specific number, down to the cent. You need a cashier’s check from your bank in that exact amount. Plan to get it the business day before closing.

What to bring to closing:

- Government-issued photo ID (two forms recommended)

- Cashier’s check in the exact amount specified in your Closing Disclosure

- Your checkbook (for any small adjustments at the table)

- Proof of homeowner’s insurance (your agent provides the binder to the title company, but have it accessible)

The Closing Day Command tab in the First Time Home Buyer Planner has a live countdown to your closing date, a day-of checklist with the cashier’s check field, a final walk-through notes section, and a post-close 30-day setup list. The preparation starts days before closing, not the morning of.

The First 30 Days After Getting Keys

The post-close period has its own checklist that most first-time buyers don’t think about until they’re already in the house:

- Change the locks — your seller has likely given keys to neighbors, cleaning services, and contractors over the years

- Connect utilities in your name (some may have been in the seller’s name at closing)

- File your homestead exemption if your state or county offers a property tax reduction for primary residences (many have annual deadlines, often January or March 1)

- Set up mortgage auto-pay and confirm the first payment date

- Update your address with the IRS, your bank, your employer, and any accounts still at the old address

- Locate your shutoff valves — water main, gas, and electrical panel locations before you need them in an emergency

The post-close list is built into the Closing Day Command tab so it’s visible alongside the closing day preparation, not something you only discover weeks later.

Frequently asked questions

- What do I need to bring to closing?

- Government-issued photo ID (two forms is safer), your cashier's check for the remaining closing costs, proof of homeowner's insurance (your insurer should send the binder to your lender), any outstanding documents your lender requested, and your checkbook for any small adjustments. Your agent will tell you the exact cashier's check amount 24–48 hours before closing — have the number tracked so there's no last-minute scramble.

- How many documents does a first-time buyer need to track during the purchase?

- A typical purchase requires 15–20 documents across the timeline: pre-approval letter, purchase agreement, inspection report, repair request and seller response, appraisal report, title commitment, HOA documents (if applicable), homeowner's insurance binder, loan estimate, closing disclosure, and the final HUD-1 or closing statement. Each one has a deadline.

- What happens if I miss a document deadline during escrow?

- A missed document deadline can delay or derail your close. The most common one is the Clear to Close (CTC) document from your lender — your lender needs every requested document before they can issue it. Delays in CTC push the closing date, which can trigger penalties in your purchase agreement.

- What should I do in the first 30 days after closing?

- The post-close checklist includes: changing the locks (your seller may have given keys to contractors, neighbors, anyone), connecting all utilities in your name, filing your homestead exemption if your state offers one (deadlines vary), setting up a mortgage auto-pay, filing your homeowner's insurance claim contact info somewhere accessible, and notifying the IRS of your new address.

- How much does the First Time Home Buyer Planner cost?

- One-time purchase of $29 on Etsy. It covers the full purchase process from offer to closing day plus the first 30 days post-close.

Ready-made dashboards

Skip setup — grab an interactive dashboard built for this exact workflow.

ListingResearchOS Shop

All dashboards — one-time purchase, yours forever

Single HTML files. No subscriptions. No login. Works offline in any browser.

Browse the Etsy Shop →